What Is a Micro-Personal Loan and How Does It Work?

Ever found yourself needing ₹5,000 or ₹10,000 in an urgent situation, maybe for a medical bill, a quick repair, or a small purchase, but didn’t want to go through a lengthy bank loan process? That’s where microloans come in. But what exactly are they? And more importantly, how to get microloans with minimal effort and hassle?

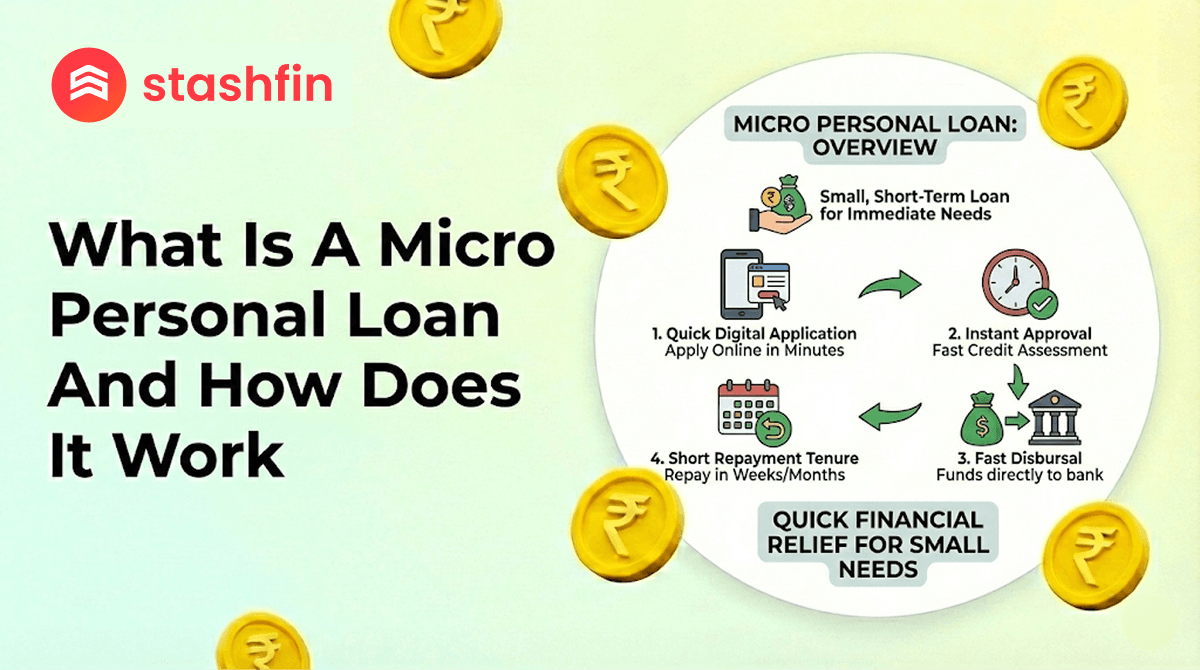

The question What is a microloan often pops up because many people still think of traditional personal loans that start from ₹25,000 and need long approval times. Micro-personal loans are an exception; they are small, fast, and easy to get. Lenders and other NBFCs offer loans from as low as ₹2,000 to ₹50,000. These are meant to be used as short-term, emergency funds and repayment options are more flexible. Within minutes of approval, the amount gets disbursed straight into your bank account.

By answering what a microloan is, this guide will explain everything you need to know, from eligibility criteria to repayment structure. We’ll also cover how to apply for a microloan, compare it with regular personal loans, and list the pros and cons. If you’ve wondered whether you can get a micro personal loan without a CIBIL check or whether a micro personal loan for self-employed individuals exists, you’ll find those answers here. Let’s explore this smart, convenient financial tool that keeps you prepared for emergencies.

What Is a Micro-Personal Loan?

Micro personal loans are a fast and convenient way to meet your unexpected bump in the road. Otherwise known as low-amount personal loans for emergencies, they’re designed to have special features for short-term needs:

- The minimum loan amount is ₹ 2,000 up to ₹ 50,000

- Fast, app-based approval, generally in minutes

- Short-term, normally 6 months, but can be up to 12 months

- No paperwork, only Aadhaar, and PAN along with minimum income proof

- Frequently, you even get it on the spot when you're approved.

These loans are ideal for small, unforeseen expenses like mobile repairs, medicine, or utility bill payments. If you're self-employed and wondering how to get microloans, Stashfin makes it easy with minimal paperwork and fast processing.

Key Features of Micro Personal Loans

Here are the standout qualities that make micro personal loans popular:

- Instant Approval: Get the loan processed and disbursed within minutes, especially on Stashfin.

- Minimal Documentation: The documentation is quite simple: Only Aadhaar, PAN, and a recent bank statement.

- Customized Tenure: Typically 3-12 months, providing the flexibility to handle shorter commitments.

- Small Amounts: With a low loan amount, it is less risky and lower interest costs than larger loans.

- Digital Process: The entire application and approval process occurs via a mobile app; no branch visits are needed.

Who Can Apply for a Micro-Personal Loan?

A wide range of borrowers can apply for micro personal loans, especially useful to those who need small, fast funds:

- Salaried individuals seeking emergency funding

- Self-employed professionals waiting for client payments (yes, there are micro personal loans for self-employed options!)

- Some lenders provide a micro personal loan without CIBIL checks to individuals with bad or no credit history.

- Homemakers, gig workers, and students provided that they have an active bank account.

- Freelancers or delivery executives in need of a short-term loan

Micro Personal Loan vs Regular Personal Loan

Both micro personal loans and regular personal loans serve the same purpose of giving you access to cash when needed, but they also have a lot of differences regarding loan amount, the application process, the paperwork process, and the repayment flexibility.

A micro personal loan is usually a small amount between ₹2,000 and ₹50,000. It’s intended to help you meet immediate, short-term costs, such as a mobile repair, medical treatment, or an emergency travel fare. In contrast, a typical personal loan works for an amount as little as ₹25,000 and can even stretch to ₹10 lakh or above, thereby fitting for bigger spending like weddings, home renovation, education, or higher education.

The documentation is another thing you might want to contrast. Unlike regular personal loans, which don’t just look for Aadhaar, PAN, and bank statements but also proof of income, salary slips, IT returns, and employment, microloans can be bagged without seeking too much more.

Microloan rates, on the other hand, usually are a bit higher at 18-25%, owing to the smaller loan amounts and shorter terms. Standard personal loans generally have lower interest rates, ranging from 10% to 15%, but are difficult to qualify for with a low credit score.

Last but not least, repayment of micro personal loans is usually shorter, ranging from 3 months to a year. Regular personal loan, in contrast, offer longer repayment periods of 1 to 5 years, giving more flexibility for large payments but also increasing the total interest paid over time.

How to Apply for a Micro Personal Loan?

Wondering how to take out a microloan? Here’s what to do, step by step:

- Choose the right lender: Find out lenders who are providing pre-approved micro personal loan offers.

- Download the mobile app.

- Complete the application & KYC: With Aadhaar, PAN, and a selfie.

- Check Eligibility: Indian nationals aged 21-60 are to be provided a basic income salary, or self-employment.

- Choose the loan amount and term: Between ₹2,000 and ₹50,000, repayable in 3-12 months.

- Upload documents: Generally, Aadhaar, PAN, and the last 3 months’ bank statements.

- Receive approval: Straightaway or within a few minutes.

- Loan disbursement: Get money in your bank account.

- Repay via EMI or bullet payment: Choose a repayment style based on tenure and interest.

Stashfin makes all that easier for you: no frequenting of branches, no need to call up any to ask, “Is a personal loan better than a microloan?” When you need cash urgently and require less than ₹ 50,000.

Pros and Cons of Micro Personal Loans

Here are the pros and cons compared with traditional personal loans or credit cards:

Pros

- Fast and quick – No more waiting for 2+ weeks or putting up with complex paperwork

- Easy in an emergency – Covers sudden expenses

- Access to Credits that aren’t Credit-Based – Perfect for Those with Bad Credit

- Goodbye, Unwanted Fees! – No security deposit, no upfront fees, and no annual fee!

Cons

- Higher interest rates (18–25%)

- The borrowing period is short and has less flexibility.

- The loan amount is limited – Not much flexibility.

- Risk of overuse – Easy access could lead to frequent borrowing

Be smart with microloans, particularly how to obtain microloans that are tailored to your needs without stretching your financial resources.

Conclusion

A micro personal loan is a handy financial tool for covering urgent, small expenses, whether you're thinking, “What is a microloan?” or how to manage a ₹10,000 emergency. With Stashfin, you can get microloans in minutes and repay within months without the hassle of large banks. But it’s important to choose wisely. Measure against rates, verify the repayment terms and make sure your income can bear the EMI. Monitor how much you borrow so you don’t get caught in a borrowing cycle.

So, when you need a little help quickly and may not want to go through a traditional personal loan process, a microloan is also a great option.